If you are employed by a new-age startup, chances are, you will be unceremoniously laid off with an average severance package and perhaps, a good letter of reference. You might be asked to put in your papers soon. One might think that something is plaguing budding Indian startups, right? Well, that is not the case. You see, over the past two years, several startups blindly hired new talent. In fact, hiring truckloads of employees became a major function of the perceived health and growth of startup businesses. Now, however, such startups have found their strategy of showcasing strength to be unsustainable.

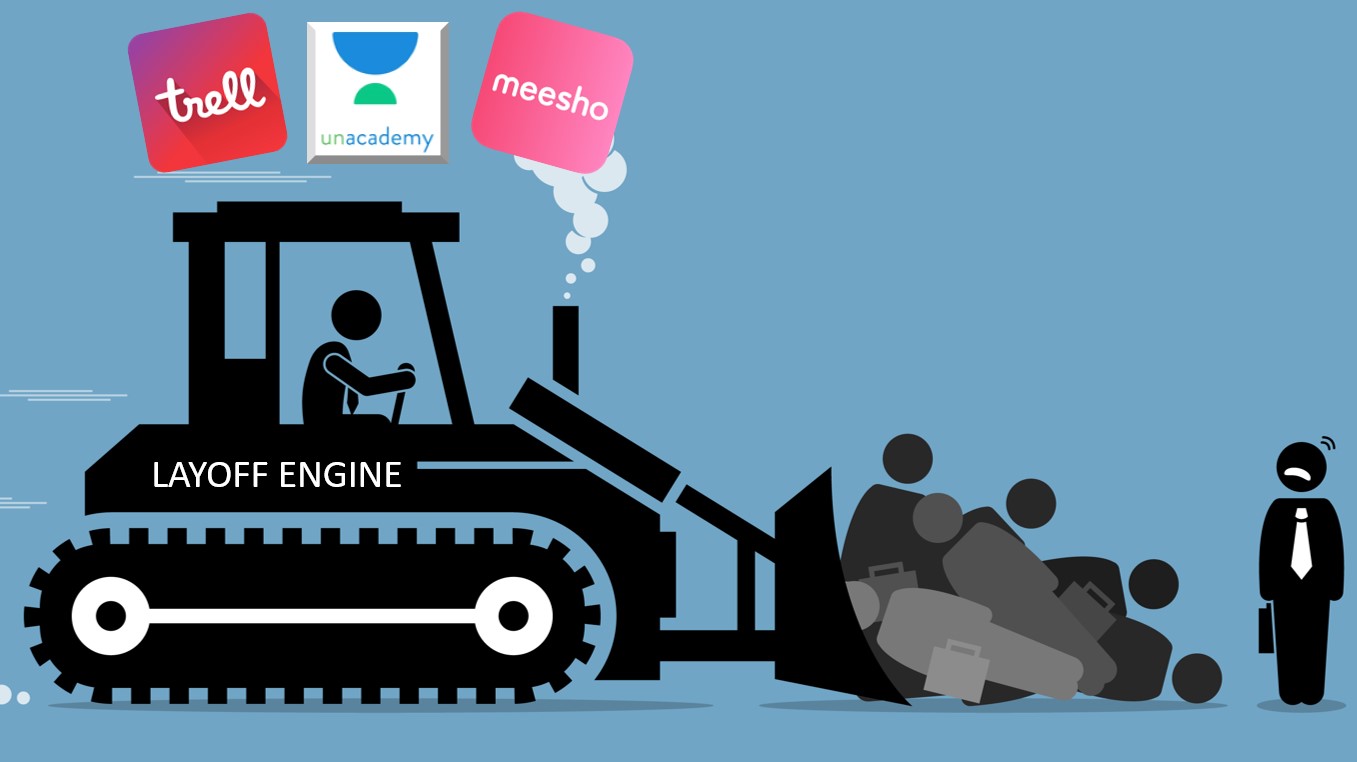

So, employees are the ones suffering, as always. In the past few weeks, over 1,700 startup employees have found themselves jobless. Leading the layoff campaign is EdTech giant Unacademy. Unacademy, India’s second-largest ed-tech firm after BYJU’s, has reportedly laid off 1,000 employees over the past few weeks in a cost-cutting drive. Interestingly though, 2021 proved to be a robust growth year for such educational startups in India, as they collectively raised close to $4.7 billion.

Unacademy, Meesho, Trell and Many More

At Unacademy, “cost restructuring” is the new buzzword. Those affected by the company’s layoff spree are mostly educators or tutors and contractual employees. Those laid-off constituted nearly 10 per cent of Unacademy’s total workforce.

Meanwhile, Meesho – a Bengaluru-based social commerce firm, has laid off about 150 employees from its grocery arm. According to the Economic Times, the layoffs have been undertaken in a bid to reduce ‘cash burn’.

Trell is a social commerce platform. The startup allows users to create content related to beauty or lifestyle products and post it on the platform. Recently, the startup let go of nearly 300 employees. Trell had incurred a loss of Rs 78.4 Cr in FY21. That was nearly a 550% increase from the losses it had incurred in FY20.

In February this year, Mumbai-based EdTech startup Lido Learning, which provided live online tuitions in small groups of six, closed down and asked its 1,200 employees to hand in their resignations.

Meanwhile, under the guise of ‘restructuring’, Furniture rental startup Furlenco had laid off close to 180-200 employees in March. Like many others, Furlenco too had ramped up its hirings in 2021. So, the layoffs came as a shocking surprise to everyone affected, showing once again how employee growth rate is not an indicator of a company’s health.

What is Leading to such Layoffs?

Investors whose portfolios are beginning to age are reportedly putting pressure on established startups to ramp up profits and give them a memorable exit. As for new-age startups, they simply want to go lean and ensure optimal performance with minimal employees. Despite hiring workers in a fit of craziness over the past two years, such startups have only now realised that they can do better if they have a small yet highly effective workforce.

Separately, many startups want to go public. According to one investor quoted by Inc42, “We see startups raising funds, having millions in the bank and then looking to diversify their revenue. While they may be confident about their business model and prospects, the reality is not always in line with this expectation.”

Read more: 2021 showered a whopping $36 billion on Indian startups

Another important factor behind startups witnessing their fortunes shifting radically in a short span of time is their overreliance on bank loans and non-customer sourced funding. Ultimately, every company must ensure that customers bring in revenue to the coffers, giving the management a degree of autonomy, particularly in the field of deciding employee strength.

It is evident that a lot of uncertainty continues to prevail among Indian startups, particularly those founded recently who happen to deal with new-age products and services.