Indian economy is all set to grow at a swift pace. The ‘twin balance sheet’ problem, identified as the major reason behind the low economic growth in the Economic Survey is getting solved. The banks in the country could not lend due to capital shortage and companies did not apply for loans because they were not able to pay back the money borrowed earlier. This was termed as ‘twin balance sheet (TBS)’ problem by the former chief economic advisor, Arvind Subramanian in Economic Survey. The Banks posted second consecutive double digit credit growth in FY 19. Bank credit grew at 13.24 percent to Rs 97.69 lakh crore in FY 19 while the deposits grew by 10.3 percent to Rs 125.72 lakh crore.

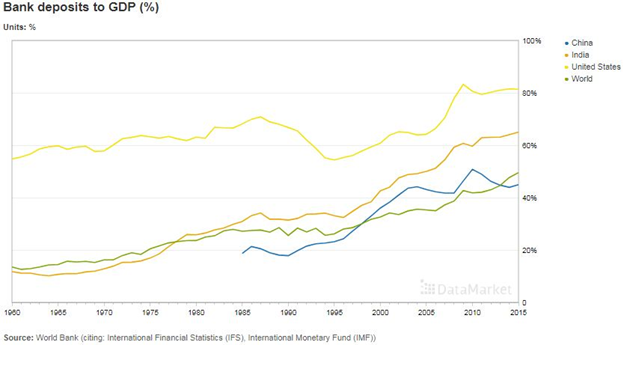

The credit to GDP ratio is around 52 percent while deposit to GDP ratio is 67 percent. The credit to GDP ratio is very low in India compared to global average of 104 percent and China’s 155 percent. The deposit to GDP ratio in the country is high compared to global average of 49.5 percent and Chinese average of 44.95 percent. So, India has better deposit rates but the credit growth is still lower due high lending rates. The previous governors of RBI (Raghuram Rajan and Urjit Patel) kept the lending rates very high even by conservative estimates. The high loan rates hurt the economy as the lending grew at very low pace and thus economic activities slowed down. RBI is considered among most conservative central banks and the cost of capital in India is very high compared to other emerging markets around the globe.

The institutionalization of inflation control through a mandate to monetary policy committee helped the central bank on the front of inflation control. Given the fact that inflation was very low, the central bank should have lowered the lending rates. But it kept the rates high which hurt the economy. When inflation reached the lower level of mandate {4(+-) 2}, RBI started reduction in rates. However the incumbent governor of RBI has been rational towards the lending rates and lowered it by 25 basis points in last two monetary policy meetings.

The bank deposits grew at 15.8 percent in FY 17, the fiscal year when demonetization was carried out. However, credit growth declined to 4.54 percent to 78.41 lakh crore rupees due to high lending rates and slowdown in economic activities. The deposits growth lowered in FY 2018 as demonetization effect withered and credit growth picked up, given the increased economic activity and low interest rates. Finally in FY 19, the economy has banking activity normalized and credit growth as well as deposit growth witnessed double digit growth.

The Modi government brought Insolvency and Bankruptcy Code (IBC) to solve NPA issue. The difficult phase for banking is over and banks got a substantial amount of money back through resolution of many bank loan cases. Central government also decided to pump money in public sector banks to increase capital adequacy. Now the things have become better and it is expected to improve further because banks have enough capital and the corporate sector is willing to take loans given the low rates. The growth in credit will result in investment in markets and therefore economic growth will improve further.