India posted one of the highest quarterly economic growth in its history with 13.5% in the first quarter of FY 23 (April-June). Although given buoyant economic activity in every sector, from agriculture to manufacturing and services, the economists and statisticians were expecting an even higher growth rate.

In the last few months, India’s direct & indirect taxes are among the highest, companies are hiring like never before, and salaries are going up exponentially. India has emerged as the only bright spot amid global turmoil, and foreign as well as domestic investors are bullish on Indian economy.

Growth in different sectors

The agriculture sector, which has remained a bright spot for India since Covid pandemic, has continued to perform excellently at around 4.5%. In the last fiscal year India – for the first time in its history – exported agricultural goods worth more than 50 billion dollars given the rising demand for wheat and rice, and growth in their prices as well.

The growth in mining sector was 6.5%. The growth of 6.5% in mining and 4.8% in manufacturing is a big jump for India where manufacturing growth has been largely stagnant in the last few years.

The consumption of electricity, gas & other utilities grew by 14.7% as the demand for power went up in summer season due to Air Conditioning demands. Also, the rise in factory activity and resume of public transport, a large part of which like Metro Trains and Railways operates primarily on electricity, contributed to huge growth in the sector.

Construction grew at 16.8% given higher demand of housing as well as commercial real estate in the last few months. Home purchase is registering record growth, especially in metropolitan cities and even in villages, the construction of pucca (concrete) houses under the various government schemes hit a new high.

The growth in construction sector is significant because it generates a large number of jobs, especially for the people at the bottom of the pyramid.

Also Read: Here is how India’s GDP growth rate compares with developed and developing world

Trade, hotels, and transport, which suffered heavily in the last two years, recorded highest gains with above 25% growth. The people across the country went on long vacations in April to June quarter as travelling was fully resumed. This brought back the main source of income to many states like Himachal Pradesh, Uttarakhand, Jammu & Kashmir and the northeastern states. Metropolitan cities have also a large number of people who are employed in the tourism sector and the resumption of contact based activities brought them back into the market.

The growth in financial, real estate, and professional services grew at around 9.2%, which is very healthy given the fact that impact a base effect (low growth in the last year due to lockdown) was minimal to this sector. Except residential real estate, this sector hardly has any impact of lockdown and it grew in near double digits. This shows the resilience and growth potential of the Indian economy.

Public administration, defense, and other services also grew above 25% as the governments across the country (state, centre, and local bodies) resumed their activities and defense procurement was also resumed.

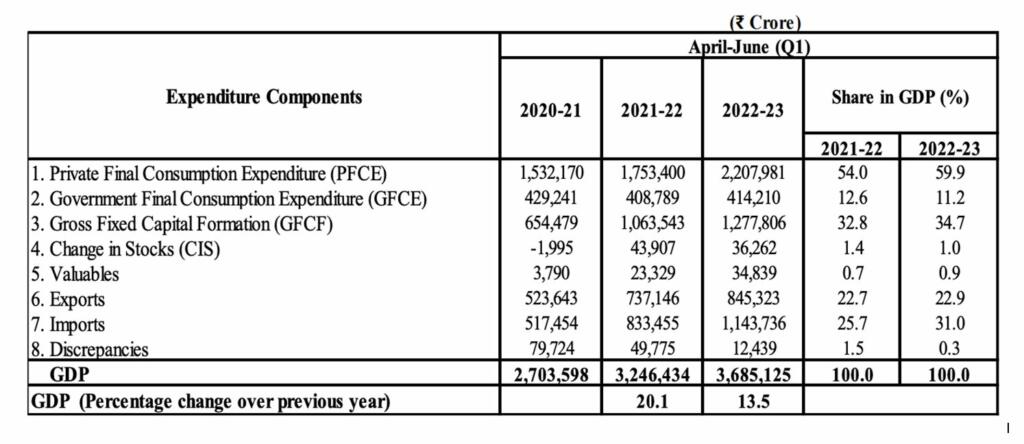

Overall, the Indian economy performed extremely well as agriculture, manufacturing, and service sectors performed excellently. Although, the GDP growth was impacted by rise in imports because the final number is calculated by adding net imports (which was in minus), final consumption, and net investment. While the private financial consumption was very buoyant and increased its share in GDP to 59.9% from 54% in the last fiscal of same year, and investment’s share also increased from 32.8% to 34.7%, this positive growth was impacted by negative growth in net imports which increased the share from ~ 25 to 31, a decline of around 6 percent.

While the imports cannot be stopped as they form critical component of many export items, the government should take steps to balance India’s trade. The imported items need to be replaced by Made in India products as it will generate employment and also contribute to GDP.

The government is bullish on economy and hopes that Indian economy will become an outlier amid ongoing global turmoil and depressed economic growth. “We (India) have zero per cent chance of slipping into recession. I hope for double-digit growth. We will work for it…..so if you are not on the verge of recession, it gives me confidence that you are constantly responsive in terms of sections which need hand-holding,” the finance minister told reporters.

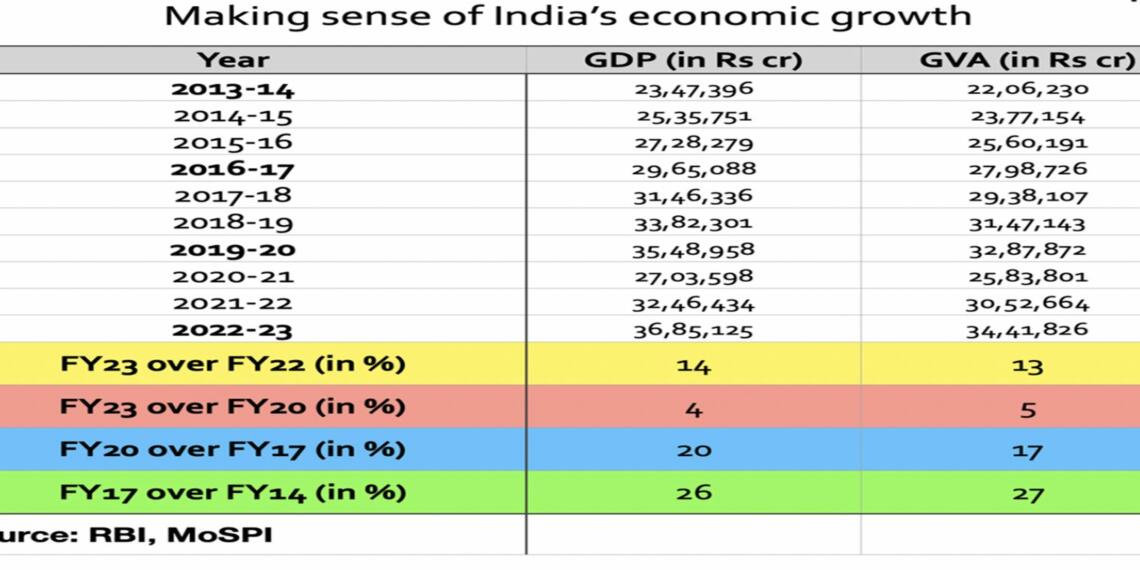

If India is able to post around 7-8% growth in next 5 years, it will overtake Germany and Japan to become third largest economy in the world after the United States and China. In the last few years, India’s stature in the international arena has continuously grown as the country handled the pandemic and many other issues of development very well. Although, the economy of 1.4 billion has miles to go to become a developed country by 2047.

Support TFI:

Support us to strengthen the ‘Right’ ideology of cultural nationalism by purchasing the best quality garments from TFI-STORE.COM