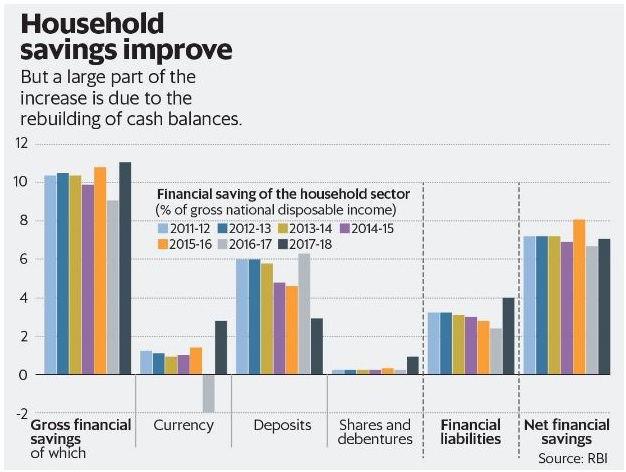

Household savings in the country has increased substantially. In fact, it is highest in the last seven years. The household savings as a percentage of gross national disposable income (GNDI) increased from 9.1 percent in 2016-17 to 11.1 percent in 2017-18. In our national accounts, household sector savings includes almost all non-government, non-corporate entities. This brings individuals, sole proprietorships businesses, limited liability partnership entities, NGOs and charitable institutions, educational institutions into the arena of the household sector. So, by and large, the household sector stands as a representative of the informal sector. Therefore, we can conclude that savings in the informal sector have increased exponentially in the last fiscal year.

This is indeed a very good news for the economy:

Household savings are the most important source of private investment in the economy. In last few years private consumption and public investment have been drivers of economic growth of the country. Private consumption accounts for almost 58 percent of India’s GDP which is highest in Asia. But the problem was that private investment had not grown since last few years, first due to slow economic growth and then due to demonetization. In the post demonetization period, government spending increased from 6.7 percent in March 2016 to 9.53 percent in June 2017. But the problem is that government could not sustain high public spending for a long period given it strains fiscal deficit targets and destabilize macroeconomic fundamentals. In previous years government could increase public spending due to low crude oil prices but it could no longer spend more because crude prices have moved northwards in the last few months. In the post-demonetization period households started to build their savings, especially cash reserves deposited in banks during noteban. The increased household savings will lead to an increase in private investment and the government will no longer need to cover it up with public investments.

The effects of an increase in household savings are visible in rising stock markets which registered above 50 lakhs new investors in the last fiscal year. Domestic investors covered up the decrease in foreign investment due to hike in US fed rates. As the chart shows, investment in shares and debentures rose exponentially in the last fiscal year. But we can see that cash is still king of household savings because households started building cash reserves in post demonetization months. As we can see bank deposits has taken a sharp southward move in post-demonetization period. The availability of cash has made it possible for households to withdraw the deposits during demonetization. Cash availability has reached to pre-demonetization level due to government’s quick efforts to solve cash crunch after demonetization.

The only problem which comes out in RBI’s annual report on household savings is the rise in financial liabilities. This may be because the restrictions on lending by public sector banks by RBI led to an increase in personal loans. To solve the NPA crisis RBI has put strict regulations on public sector banks on corporate lending. However, the silver lining is that net financial savings have increased despite the rise in financial liabilities.

As the RBI report points out “As per the Bank’s preliminary estimates, net financial assets of the household sector increased to 7.1% of GNDI in 2017-18 on account of an increase in households’ assets in the form of currency, despite an increase in households’ liabilities.” So, increased household savings will lead to spur in private investment which will result in higher economic growth in upcoming months.