The more time you have, the more you procrastinate things. This is why most of us study for exams and pay credit card or mobile bills only a few days (or hours!) before the D-day. This is also the reason that why most of the people make (or think about) tax-saving investments only in the last three months of the financial year when their company’s HR department ask for investment proofs.

However, needless to say, deferring the tax planning or procrastination is not a good idea, especially when it comes to choosing tax-saving investment options. These avenues not only save tax, but also grow your wealth in the long run.

Therefore, to make the best use of these investments, it is essential to start your investment as soon as the inception of the new financial year.

However, all is not lost if you haven’t planned yet. Ditch your procrastination habit in the next year, and for this year, there are ways to save tax in last three months:

Before initiating the tax-saving process, compute your taxable income that needs to be invested. If you are a salaried professional and contributing towards the employee provident fund account, your taxable income would further go down.

Now let’s discuss ways to save tax. Among the available tax-saving investment options, we have handpicked some of the best for you:

- ELSS Funds

ELSS or Equity Linked Saving Schemes are mutual tax-saving funds which come with the lowest lock-in period of three years and the potential of yielding high returns among other investment avenues of Section 80C. Moreover, ELSS funds do not need recurring payment, and therefore, if you realise that your funds are not giving you expected returns, you can stop making further payment without paying charges. With ELSS, you get an opportunity to make a systematic investment without timing your entry into the market.

Tax Benefit: Up to Rs 1.5 lakh under Section 80C

- Health Insurance

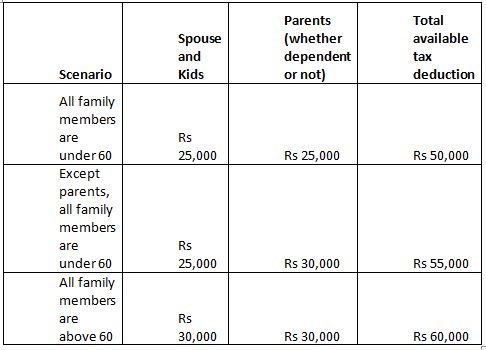

Though, buying health insurance just to get tax benefits is a complete no-no, it is a high time you consider both the benefits—tax benefits and your financial coverage—in one product and purchase a health insurance policy. Go with the best Mediclaim policy to get coverage against soaring medical expenses. A health insurer covers both pre & post hospitalisation expenses and ensures that you get good medical treatment without worrying about treatment expenses. In addition to buying an individual health insurance, you can buy a Mediclaim policy for your family as well and get the following tax benefits:

Tax Benefit: Up to Rs 25,000 in case of policyholders below 60-year and Rs 30,000 in case of people above 60 years under Section 80D.

- Term Insurance

A term insurance is meant for your family and not for you. As the insurance policy pays a fixed sum assured to your family in case of your death, it gives the financial security to your family even in your absence. However, in case the policyholder survives the tenure, nothing is paid, i.e., there is no maturity value. The tax benefit is available for both premiums and death benefits received by the family.

Tax Benefit: Up to Rs 1.5 lakh under Section 80C

- Tax-Saver Bank Fixed Deposits

Mainly conservative investors who do not want to take risks with their money can invest their money in five-year bank fixed deposits. As the money is locked in for five years, premature withdrawals are not allowed. Though the investment in fixed deposits along with income earned from them are tax-free, you would have to pay tax on the returns earned during the accumulation phase.

Tax Benefit: Up to Rs 1.5 lakh under Section 80C

- PPF Account

It is a traditional investment avenue which has invested money for 15 years. The deposits in PPF can be either done in maximum 12 instalments or lump sum. Even though there is a lock-in period of 15 years; partial withdrawals are eligible for the 7th year. Since PPF comes with EEE status, premium, maturity amount and the returns generated are tax-free.

Tax Benefit: Up to Rs 1.5 lakh under Section 80C

Conclusion

Though, as a late planner, you would not be able to get the maximum benefit from your tax-saving instrument, it would be possible to minimise the damage. While, you are making all investments to save tax, do consider your age, risk returns, liabilities and dependents before investing. The most important thing—Don’t procrastinate your tax planning in 2018-19!