I wanted to write the heading as a tale of two cities and start with opening lines of the epic book. However, I believe this Budget2016 needs to looked from multiple perspectives hence I have kept the title as Vantage Point. I am trying to put out an exhaustive write up on the Budget2016 from 3 vantage point viz.,:

- From the country

- From the businesses (corporates paying tax)

- From individuals (or salaried class)

Firstly, lets be honest, the Budget2016 exercise has come in a tumultuous time. The world economy is slowing avenues of growth have seen a shrinkage. While, the government has been able to maintain a GDP growth of 7.5%, the future looks uncertain. Given this scenario, the Finance Minister and as reiterated multiple times by the RBI Governor has stuck to fiscal discipline. In fact, the government has tried to spend in its (revenue collection targets seem bit ambitious), means in the key pain points i.e. rural, agriculture & infrastructure, from a nation’s perspective, it is a structurally positive Budget. The heartening thing is that fiscal deficit target is maintained, which is very positive from investors, credit rating, nation and currency point of view. A slip in this ratio would have cause further currency carnage and deterioration of bond yields. Having said that, this article looks the Budget2016 from Holistic perspective. Mind you, this article is lengthy and would appreciate that reader have a complete reading. It is a Budget primer as well points out to certain serious issues in taxation, which needs to be looked at as well.

Lets start from the country perspective and Budget2016 numbers:

Country perspective means from India, and people who are rating India and people who will benefit from the expenditure planned by the government. As a mentioned in my earlier piece, that the Budget2016 is structurally positive for the nation as a whole. This statement is on the back of three key pillars:

- Maintaining fiscal deficit target

- Enhancing spend on agriculture, infrastructure

- Maintaining tax collection buoyancy

Fiscal Consolidation

The government has targeted to reduce the fiscal deficit to 3.5% of GDP in FY17BE from 3.9% of GDP in FY16RE, in line with the fiscal deficit target set under the medium-term fiscal policy framework. The deficit math seems bit optimistic, as it based revenue receipts from telecom spectrum auction (Rs. 50,000 cr.), inadequate clarity on seventh pay commission wage hikes for central government employees, and divestment receipts (divestment work just handed over to NITI AYOG).

Lets put simply how the government plans to meet its expenditure & sources of income

Revenues

![CropperCapture[2]](http://static.tfipost.com/wp-content/uploads/2016/03/CropperCapture2.png)

Expenditure

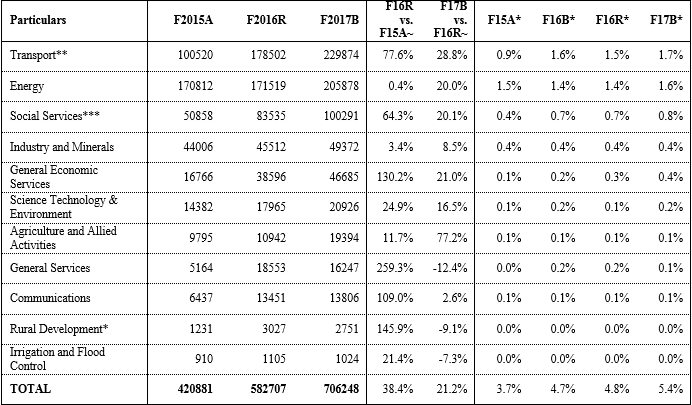

Of the above central government allocation of INR 308110 cr., further, Rs. 389139 cr., shall be raised from Internal and Extra Budgetary Resources of Public Enterprises, etc., which shall take total spending on plan items to Rs. 706248 cr. Accordingly, key heads for spending shall be as under:

Note: *Includes the provision for Rural Housing but excludes provision for Rural Roads, **Includes the provision for Rural Roads, ***Excludes the provision for Rural Housing

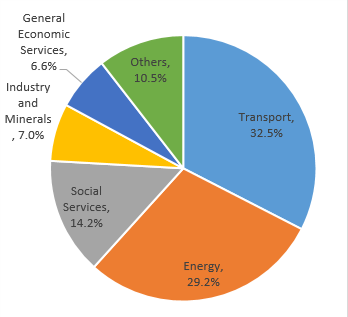

The government has stepped up spending in the transport sector i.e. roads which is contributing the highest of the overall spending. The overall spending is expected to be as under:

Of the total transport sector spending, the government is targeting INR 97,000 spend for road including Pradhan Mantri Gram Sadak Yojana with ~100 KM per day target. The road sector allocation includes spending for rural roads. The overall allocation planned for rural sector is ~INR 87,765 cr.

The transport, energy and social sector spend together aggregate for 75.9% of total spending. In fact, energy & transport i.e. Piyush Goyal and Nitin Gadkari have cornered ~61.7% of total plan spend.

Further, the agriculture, rural & irrigation sector combined is expected to grow at 54%.

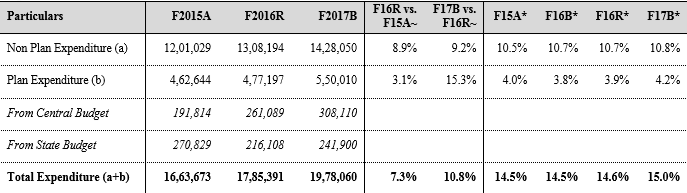

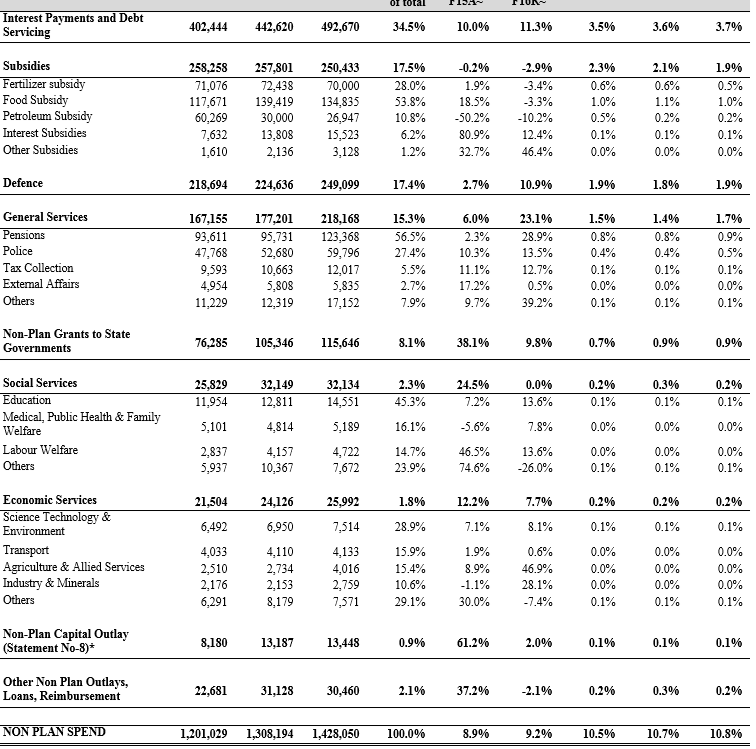

Non Plan Expenditure

The non-plan expenditure contributes the major spending planned by government. The broad heads are as under:

The key spend heads aggregating for major share of non-plan expenditure are:

- Interest & debt repayment (34.5% of total spend)

- Subsidies (17.5%)

These two account for ~52.5% of total spend. In fact, of the major components of subsidy, Food Subsidy is the highest with Rs. 250,433 cr., where there are inefficiencies of ~Rs. 1,00,000 cr. which translastes to ~0.90% of GDP. Improvement in this shall help us rationalize tax burden. In fact, Rs. 100,000 cr., of efficiency is ~9% of Gross Tax Revenues. There needs to be concentrated effort improve the overall spend.

One of the key spend in the ensuing year shall be Pension, which is expected to increase by 28.9% in F17B vs., only 2.3% in F16R. This is primarily on account of OROP impact.

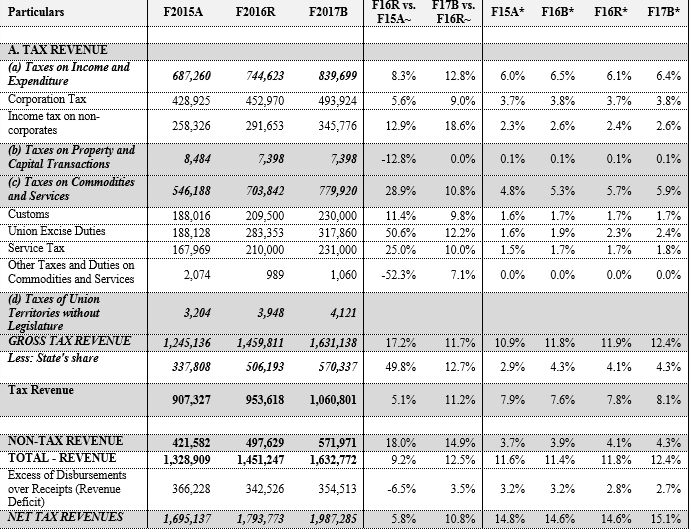

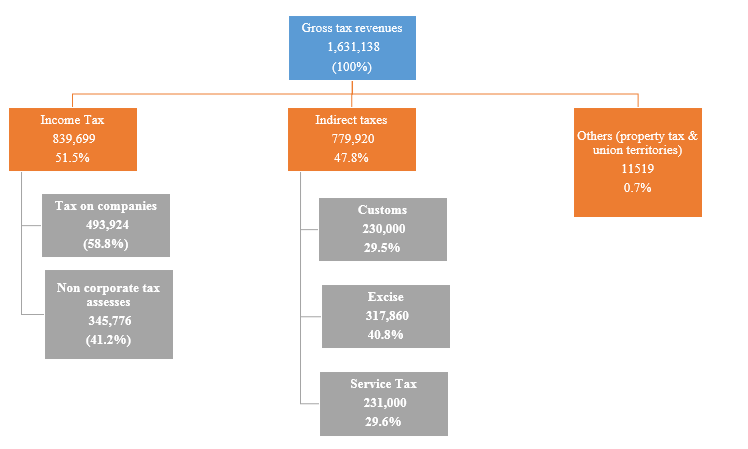

The government has announced a scheme similar to VDIS scheme, wherein upon payment of aggregate tax of 45%, any person can bring his black money into books. The FY16E gross tax revenue is expected to be 10.8% of GDP, while for FY15e, it was 10.0% of GDP. Key tax numbers as % of GDP are expected to be as under:

Note: ~ YoY growth, * as a % of GDP

The government has seen a seen a 5.8% growth in overall net tax revenues in F16R, while for FY17B it is Budgeted to increase at 10.8%.

- The government expects highest growth to come from Personal Taxes or non-corporate assesses primarily on the back on Seventh pay commission increase in salaries leading to higher TDS, new voluntary disclosure scheme and taxation on dividend in the hands of recipient.

- Service tax is expected to grow at ~10%, since there is no new service additions in the net, and the rate of tax expected to be same, this is a conservative assumption.

- Excise duty revenues are expected to grow at 12%, since there is no major Excise duty hike, a 12% growth is adequate.

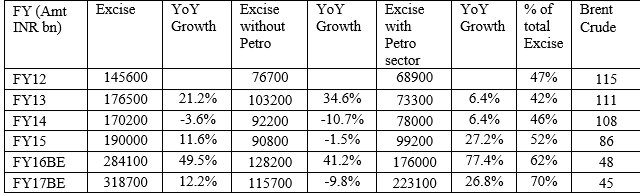

In F15 and F16, while the growth of collection in Excise duty from Petroleum sector has outpaced the overall excise duty collection rate. In fact, in F16R, the excise duty from petrol is ~62% of total excise collection and in F17 this ratio is expected to increase to 70%. It is noteworth that despite an expectation of increase in overall excise duty, the government expects non-petroleum excise duty to witness a de-growth. This is worrying factor. It seems the burden of better tax collection rests on the shoulder on individual tax payers.

4. Further, the government expects Rs. 74,200 cr., to come from spectrum auction and disinvestment proceeds. This number is bit higher. Already telecom companies are facing reduction in ARPUs, and further auctions and Reliance JIO coming in; this expectation can suffer. This translates to ~0.6% of GDP.

Above figures, amount in Rs. crore

Given the above scenarios and numbers the key positives and negatives are:

| Positive | Negative |

| Fiscal deficit target set at 3.5% of GDP in F2017 vs. 3.9% of GDP in F2016 | Optimistic assumption on non tax revenue receipts from telecom spectrum auctions |

| Focus on public infrastructure maintained, with Budgeted expenditure on infrastructure segments to rise by 16%YoY. Including extra Budgetary support, infra investment spending is expected to go up by 24%YoY | Optimistic assumption on divestment target set at INR 56,500 cr., for F2017 |

| Focus on agriculture investment by creating a long-term irrigation fund at NABARD | Increase in government employee wages and pension expenditure on account of seventh pay commission recommendations is not fully provided for in the Budget2016 |

| Subsidy spending Budgeted to decline to 1.7% of GDP in F2017 from 1.9% of GDP in F2016. | PSU bank recap funding kept at Rs. 25,000 cr, which we believe will not be sufficient |

| Tax amnesty scheme for individual tax payers | Imposing Krishi Vikas Cess of 0.5% on all taxable services |

| Statutory backing for Aadhar to ensure direct transfer of benefits | No immediate cut in the corporate tax rate. Corporate dividend income now attracts an additional 10% tax |

| Introducing a new dispute resolution scheme, to ensure stable and predictable tax regime. | Un-necessarily taxing EPF at withdrawal with further complexities of annuity schemes. |

Source: Research, Morgan Stanley, News articles

Key Positive Themes

| Infrastructure Capex | Infrastructure capex allocation (through the Budget2016 and via market borrowing) has increased to 2.8% of GDP in F2017 vs. 2.5% of GDP. Measures proposed include:

1. Reforms in FDI in insurance pension, asset reconstruction companies, 2. 100% FDI in marketing food manufactured products 3. Revitalizing PPP, 4. Amendment to the motor vehicles act to open up the road transport sector 5. Revival of unserved and underserved airports in partnership with State Governments 6. Spurring gas production through calibrated marketing freedom and 7. New policy for managing government investment in public sector, including disinvestment and strategic sales. |

||||||||||||||||||||||||||||||

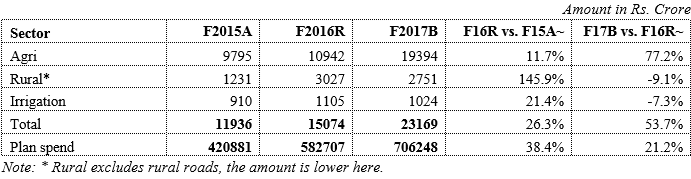

| Rural sector | To support rural credit, the government has allocated Rs1,000bn (0.7% of GDP). For developing rural infrastructure, the proposed measures are to put irrigation projects on fast track, set up longterm irrigation fund with a corpus of Rs200bn under NABARD, electrify 100% of villages by May 2018, develop 300 rurban clusters. etc. The government has maintained the allocation towards the rural job scheme MGNREGS with expenditure to GDP holding steady at 0.3% of GDP (Rs385.bn).

Expenditure on rural development:

Amount in Rs. Crore

The table shows a the allocation to rural housing is stepped by 35% in line with mission for Housing for all. Further, the above expense does not cover rural roads and rural power sector reforms.

|

||||||||||||||||||||||||||||||

| Social Services | The Budget2016 for the social sector includes schemes focused on health care, education, enhancing skills and job creation. In particular, the Budget2016 allocates Rs. 1,51,500 cr., (1% of GDP) for education and health. Key steps introduced in the Budget2016 include a new health protection scheme, a focus on quality of education under sarva siksha abhiyan, and setting up a board for skill development certification. |

The above measures, with proper implementation shall be key in boosting the rural economy and agriculture sector which is critical for growth of the nation tackling a long term problem of urbanization.

The section was pretty much a highlight on Budget2016, sources of income, expenditure and also meant to give the reader an understanding on the overall financial framework of the nation.

Lets turn to two more aspects:

- Taxation of corporates

- Taxation of individual

I will come to taxation of individuals last, and cover corporate taxes and changes in the indirect taxes section first.

CORPORATE TAX

Lets first have a look at key changes in provisions:

- No change in the corporate tax rate except for new eligible manufacturing companies which are taxable at 25% without claiming specified deductions, allowances, depreciation, and companies having a turnover or gross receipts not exceeding INR 5.0 cr., taxable at 29%. No point in doing this.

- LTCG derived by non-residents from the transfer of shares of a closely held private limited company are taxable at the rate of 10%

- Equalisation levy of 6% is applicable on the consideration payable to non-residents not having a PE for online advertisement or similar specified services. These provisions are applicable if the aggregate amount payable exceeds Rs. 1.0 L p.a. Correspondingly, such income would be exempt in the hands of the non-resident recipient. This, will impact payment to be made by Indian companies hosting websites or servers via Google.

- Supporting startup: 100 per cent deduction for a period of 3 consecutive years out of the initial 5 years for eligible ‘startups’ which are set-up before 1 April 2019 and whose turnover does not exceed INR250 Million in any FY from 1 April 2016 to 31 March 2021. Frankly, this is pretty pointless. Most of startups are new companies don’t make money initially. This is an ornamental provision. Plus, the fine print would contain conditions that will make it more difficult.

- A buy-back tax is applicable to any buy-back of unlisted shares under the provisions of Companies Act, 1956 and is not restricted to Section 77A of the Companies Act, 1956. The rules are to be prescribed to compute the distributed income under different scenarios, including shares issued under tax business reorganisations and in different tranches. The amendment is to be applicable from 1 June 2016. This section shall negatively impact buyback in case of Private Equity funds and will hamper the IRR.

- The exemption from DDT on the distribution made by SPV to REIT/ InvITs where REIT/ InvITs hold 100 percent of the SPV, would be available only with respect to the dividend distributed out of the current income and not on dividends paid out of the accumulated profits prior to the acquisition of SPV. This section pretty much is useful for REIT Developers and primarily hyper rich developers like DLF, Pancshil Realty, Phoenix Market City, etc., who have huge leased asset portfolio. It is a step in right direction, but regulation pertaining to REIT should be reduced / relaxed for even Tier 2 developers can come in its ambit. This section right now, is meant to give undue benefits to REITs.

- A new pass through taxation regime has been introduced for a securitisation trust set-up in accordance with the SARFAESI Act. Income of a securitisation trust shall continue to be exempt and any income from such a trust would be taxable in the hands of the investors. This was a much needed amendment given the state of NPAs. In fact, this amendment will be go long way improving investor IRR for investment in ARC. I will be doing a separate piece on state of ARC and how it pretty much is helpful for large borrowers only and lot needs to be done by Government on this front.

- Voluntary disclosure scheme with 45% tax rate. This is nice, given that government is without money now, so time to ask people to declare their wealth. However, this 45% tax rate will be quite a hindrance. Market rates are much lower.

- No deferment of GAAR. It shall apply from 1 Apr 2017. This is really wrong, it’s a mistake of past, that needs to be wiped out. There are better ways of collecting tax then trying to trample with investor confidence.

- Rationalization of certain tax incentives:

a. Profit linked deduction on eligible business of infrastructure facility (road, rail system, highway project, port, airport, etc.), developer of a special economic zone and production of oil and natural gas, to be available only if the specified activity is commenced on or before 31 March 2017.

b. Profit linked deduction of 100 per cent provided to the business of developing and building affordable housing projects approved by the competent authority before 31 March 2019. The minimum land area specified for metro is 30 sq. mt and for non-metro is 60 sq mt or say 645 sq. ft. We are strongly against this provision. Firstly, the developer is selling an affordable house at low margin. If this is what the governemtn is thinking, then well they are high. The affordable housing is nothing but a small house which has a ticket size of say ~Rs. 20L to Rs. 50.0 L. And, the developer makes ~25% to 40% profit even in affordable housing project. So, there is no point in giving him benefit. In fact, they government may tax them lower say at 10% or at MAT Level and benefit of the balance monies should be afforded to home buyer by way of Interest subvention. We strongly object to this provision.

c. To avail benefit of tax holiday, units in SEZ need to commence operations on or before 31 Mar 2020. Firstly, I am against this whole thing or removing tax benefits and reducing tax rate. India is not a country with a wide tax base. In fact, the government should rather strive to reduce tax burden on individual salaries personnel or the middle class who spend their life paying EMIs, investing in mutual funds, insurance policies, rather than reducing corporate taxes. Just because the SEZ policy was not well implemented does not mean the government should remove. You cannot look at each thing from a perspective of revenue foregone. The revenue foregone has created bulk of jobs in a particular area. This would have been possible had the company operated in the same area where it was. So, keep the taxes where they are, remove burden from the middle tax payer and then move to reducing corporate income tax. In fact, if we look at the tax collection numbers in the first section, the government expects majority tax growth to come from non-corporate assesses rather than companies.

d. The accelerated depreciation under Income-tax Act will be limited to 40% from 01.04.2017. This was at 80% earlier This is negative for industries like solar. - Smoothening of overall tax administration, with reduction in discretionary powers in the hands of ITO. These changes shall go a long way in reducing tax terrorism and reducing hardship on tax payer.

Lets look at the key corporate tax numbers

The Income-tax Department received 5,82,889 corporate returns electronically up to 30.11.2015 for the FY2014-15 [AY2015-16]. These returns constitute about 90% of the total corporate returns expected in financial year 2015-16.

| Corporate tax liability | 298205 |

| Dividend distribution tax | 32262.95 |

These 582889 companies can be segregated in three sections as under:

Firstly, I don’t agree with this effective tax rate being claimed as 24.7% to be right benchmark. The CBDT or Government is comparing apple to oranges. The Income Tax act has its own way of computing profit. In fact there are many expenses that are disallowed and certain case expenses are allowed at higher rate than normal book keeping. For example, depreciation rates are higher in case of Income Tax and lower in case of Companies Act, so taxable income due to depreciation impact is lower in Income Tax then the Companies Act. But, this does not mean that I take the lower tax computed in Income Tax and pay only that portion. There is something called as MAT which is to be paid if you have lower taxes and then the most important is deferred tax asset and liability. This DTA/DTL will ensure that you end you paying higher tax initially despite having a lower taxable income and you will get its credit in future. But, the point I want to drive here is that this assumption of 24.7% tax rate is comparing apples and oranges and cannot be a benchmark. In fact, by that logic, the governemtn should increase tax and reduce it from the individuals.

Indirect taxes: A new Cess-Pool

Cess-pool is a negative connotation but that’s what government has done with:

- Krishi Vikas Cess on all taxable services at 0.5%, taking the overall service tax rate to 15.0%

- One important change in excluding services from service tax net is that for houses less than 60 sq. mt., service tax shall not be applicable. This shall reduce price of houses by ~3.0%.

Key changes in excise duty

- About 13 different types of cess are now remove and well we have few new cess and excise duty

- Readymade garments with retail selling price of more than Rs. 1000 shall have 2% Excise duty (without cenvat) or 12.5% duty (with cenvat). So, now no more buying Arrow, Louis Phillpe, etc., back to Peter England.

- Clean energy cess applicable on coal, lignite and peat at Rs. 400 per tonne (increased from Rs. 200 per tonne). This can marginally increase power cost

- Infrastructure cess on passenger vehicles from 1% to 4% depending on category of car. After reading this, I was like seriously. Tomorrow, government will start charging cess on probably water, or what.

- Mineral water, soft drink excise duty hiked from 18% to 21%. Good move, after cigarette next in line.

Budget2016 – Despite the hike in excise duty or newer cess, the overall excise duty collection by the government is expected to dip if remove the petro related excise collections; in fact overall increase in excise duty collection is expected to be only 12%. There seems to be some disconnect in the government action or they growth in excise duty collection is under-assumed.

Individual taxation

Key changes / points

- No change in the income-slabs, tax rates and cess for individuals

- Surcharge to be increased from 12% to 15% where income exceeds INR1.0 cr per annum.

- Rebate from tax to be increased from INR2,000 to INR5,000, for resident individuals with total income below INR500,000

- Employer contribution to RPF in excess of INR150,000 per annum now taxable. Tax exemption on withdrawal now limited to 40 per cent of accumulated balance attributable to contributions made on or after 1 April 2016 by an employee. Salary limits to be separately prescribed for employees excluded from tax on such withdrawal.

- Tax exemption now available for 40 per cent of the amount payable at the time of closure or opting out of NPS. Amount received by nominee from NPS on death of assesse to be considered wholly exempt from tax.

- Additional deduction of INR50,000 per annum towards interest on housing loan, for loans upto INR 35L (sanctioned during FY 2016-17), where the value of the house is less than Rs. 50.0 L and where assessee does not own any other house property on the date of sanction of loan.

- Presumptive taxation scheme extended to professionals: In order to rationalize the presumptive taxation scheme and to reduce the compliance burden of the small tax payers having income from profession and to facilitate the ease of doing business, the presumptive taxation regime proposed to be extended to professionals having gross receipts not exceeding Rs. 50 lakhs in the previous year at a sum equal to 50% of such gross receipts.

- Limit for deduction of rent paid, where assesse does not own a house and does not receive HRA, increased from INR24,000 per annum to INR60,000 per annum.

- Gross Dividend would be taxable in the hands of recipients: The income by way of gross dividend, to be chargeable to tax in the case of an individual, Hindu undivided family (HUF) or a firm, who is resident in India @ 10%, if the same is in excess of Rs. 10 lakh.

This is turned out to be an Achilles’ Heel, frankly. Firstly, there was no change in income tax slab. People well were OK with that, but now the government has jumped to tax EPF contribution. This is incorrect frankly. These are the individuals life time savings. This money will be used by governemtn for lot of expansion projects etc., and subject to a paltry 7.5% to 8.0% interest. India does not have robust social security network. In fact, the most honest tax payers in India are salaried people, because there is nothing to hide an in fact, and they have no deduction. In fact, the section 80C of income tax saving is so clobbered with so many heads fighting for that Rs. 1.5 L deduction, its pointless. We strongly believe that this provision of EPF should be rolled back and in fact the deduction limit under 80C should be increased. The government is planning to reduce corporate income tax on a flawed assumption of effective tax rate of 25%. I am seriously saying it’s a flawed assumption. We are awaiting further clarification on EPF based on the Budget2016 debate and shall put out a separate analytical piece on the EPF provision itself.

I am working on a detailed piece which breaks the entire income tax statistics into more details and explains why it is futile even running around collecting higher tax from salaried people less than Rs. 10.0 L slab.

Our next two piece continuing the Budget2016 theme shall be:

- EPF – End Game

- Rationalizing tax base.