Throughout the last few decades, Public Sector Banks have proven to be one of the toughest institutions to breathe enthusiasm into. Neither the top management nor people at the bottom of hierarchy were ready to mend their ways. Apparently, the overhaul requires a massive project. With EASE, Nirmala Sitharam is reviving PSBs like never before.

Big data in banks

According to a report by The Economic Times, state-run banks are integrating all data sources. Dedicated verticals for big data and analytics are being created. The decision is aimed at infusing a data-driven approach in banking institution’s decision making. Ultimately, a data-driven approach will make it easier to recover loans, detect and mitigate fraud related cases.

Additionally, the downsizing of digital bureaucracy will assist in availing loans by retail customers and micro, small and medium enterprises. An executive contacted by the newspaper said, “Banks will expand the portfolio of end-to-end digitalised banking services and introduce digital banking solutions for value chain financing,”

Transformation through EASE

The initiative is a part of reform strategy by the Government of India. It is termed as Enhanced Access and Service Excellence (EASE 5.0). As the name suggests, this initiative was aimed to make it easier for people to access banking services in both big cities and hinterlands of the country. To expedite the process, improving the health of PSBs was the most imminent challenge faced by the Modi government.

The dilapidated state of Public Sector Banks was the worst legacy of UPA 2.O which the Modi government inherited. While PM Modi’s Ministry of Finance inherited 9.6 per cent gross NPAs, the Jaitley led Ministry did well to reduce it to 10.5 percent by the end of 2017-18. Containment was good, but eventually, it had to be brought down to zero so that banks could start lending. Clearly, a coherent policy which could solve ground-level problems was required. True, IBC and other initiatives to prevent the crisis from escalating were present, but devolution of money to the last entrepreneur is always the need of the hour.

EASE 1.0 lessened the burden of NPAs

Keeping aforementioned points in mind, the Modi government launched EASE reforms in 2018. The government knew that the dilapidation of PSBs took some time to come, so they planned to improve their health in a phase wise manner. In the EASE 1.0, the Finance Ministry decided to focus solely on minimising the NPA crisis in the country. Within a few months, a drastic change in the percentage of NPAs was witnessed.

EASE 2.0 was remarkable

To measure the progress made on these metrics, an EASE reform index was launched. The index was based on 120+ objective metrics in addition to the aforementioned themes. Currently, the index combines more than 140 metrics. On this index, Banks scored 49.2 out of 100. Encouraged by the result, the government launched EASE 2.0

In many ways, EASE 2.0 was the first stepping stone towards fulfilling the original goal of introducing EASE, which was to make banking easier for the population. The second phase focussed on Responsible Banking; including Customer Responsiveness, Credit Off-take, PSBs as UdyamiMitra (SIDBI portal for MSMEs’ credit management), Financial Inclusion & Digitalisation, and Governance and HR.

In many ways, EASE 2.0 was the first stepping stone towards fulfilling the original goal of introducing EASE, which was to make banking easier for the population. The second phase focussed on Responsible Banking; including Customer Responsiveness, Credit Off-take, PSBs as UdyamiMitra (SIDBI portal for MSMEs’ credit management), Financial Inclusion & Digitalisation, and Governance and HR.

The results were satisfactory to say the least. 140 per cent increase in financial transactions through mobile and Internet banking channels was observed. Despite an increase in the offline services made available by PSBs, the adaptability of Internet banking increased. Banks also increased the number of their dedicated marketing employees which made consumers aware about products offered by the company. Bank of Baroda, State Bank of India, and erstwhile Oriental Bank of Commerce turned out to be major performers. Average score by Banks increased from 49.2 in EASE 1.0 to 67.4 in EASE 2.0.

Also Read: Best news of 2021: Indian Banks have finally weeded out the NPA mess

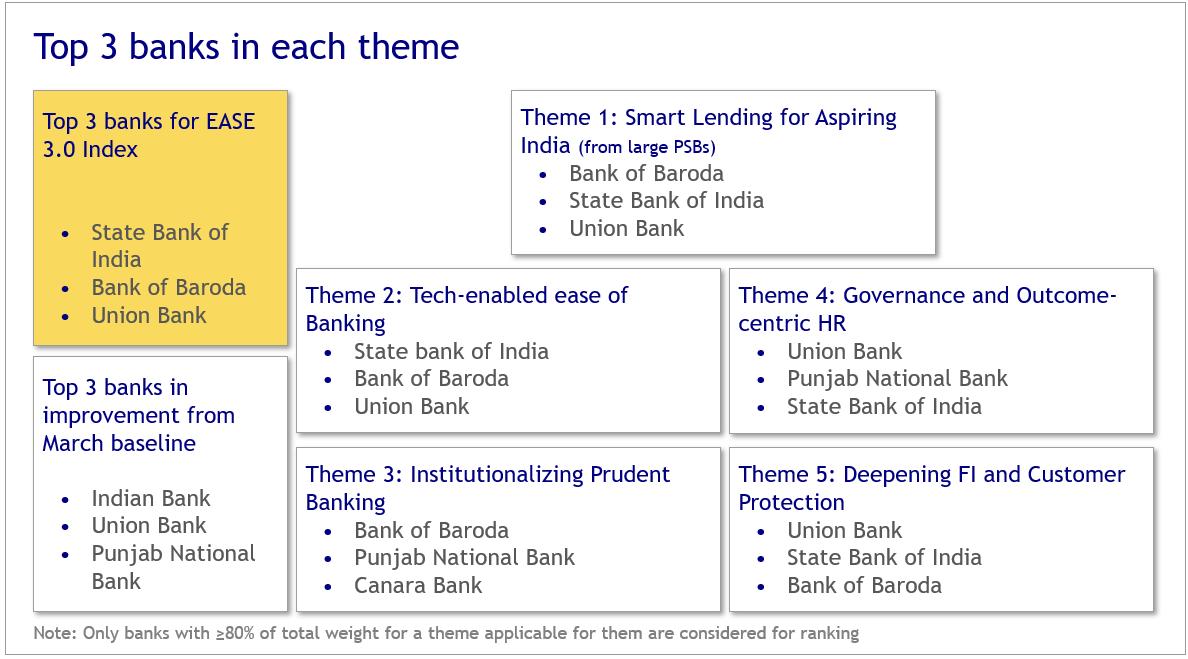

Ease 3.0 was Ram Setu

If EASE 2.0 was a stepping stone, EASE 3.0 became the Ram Setu of digitalisation of banking ecosystem. The third phase was aimed towards tech-enabled banking. Nirmala Sitharaman led Ministry aimed at paperless and digitally-enabled banking. The theme included responsible banking, PSBs as Udyami Mitra, customer responsiveness, credit take-off, and deep financial inclusions.

The initiative enabled nearly 4.4 lakh customers to benefit through simplified credit access. In the FY2021, digitalisation helped generate loan leads worth of Rs 40,819 crore. Availability of call centres, Internet banking, and Mobile banking in 14 languages played a major role in it. The portfolio included fresh personal, home and vehicle loans. Not only through loans, but digitalisation of PSBs also helped in increasing the value of digital transactions in PSBs. 72 per cent of PSB transactions were found to be taking place through digital channels.

Authority along with responsibility in EASE 4.0

After securing Internet penetration, the Finance Ministry moved on towards making services more inclusive under EASE 4.0. It aimed tech-enabled, simplified, and collaborative banking. Under it, the Finance Ministry targeted new-age 24×7 banking with resilient technology. Additionally, focus on increasing banking services in the North-East was also a key theme of EASE 4.0.

Moreover, now that Banking was in health, Finance Minister Nirmala Sitharaman found it fitting to kick off the process of giving licences to Bad Bank. Bad Bank would buy all bad loans and other illiquid holdings. The proposal of sucking up remaining NPA pressure provided leeway for allowing the banks to raise funds from outside the Banking sector.

The relaxation to PSBs did not come in vacuum as they were asked to participate in India’s development trajectory. They are now required to contribute to the ‘one district, one export’ agenda. All banks have now come out of RBI’s Prompt Corrective Action (PCA). Now banks are not reluctant to lend which is manifested in their credit numbers as well.

4 stages of EASE reforms have enabled PSBs to invest in new-age capabilities. It is like a dream come true for them since lots of them were merged to improve efficiency. Now, there is a need to privatise them. For that, a radical change in efficiency was needed and it arrived in the form of EASE reforms. Maybe, the need for privatisation will be eliminated altogether.

Support TFI:

Support us to strengthen the ‘Right’ ideology of cultural nationalism by purchasing the best quality garments from TFI-STORE.COM

Also Watch: