In the last few years, UPI has emerged as the biggest financial technology sector innovator not only in India but in the world. India became a global leader in digital payments riding on the UPI wave and now countries around the world want to emulate India’s example in the fintech sector.

UPI is an instant real-time payment system launched by the Government of India to facilitate hassle-free digital transactions. The interface is regulated by the Reserve Bank of India and works by instantly transferring funds between two bank accounts on a mobile platform. It is an umbrella organisation for all public and private retail payments in the country.

The major private players which operate on UPI are Paytm, PhonePe, Amazon Pay, and Google Pay, and the public sector player is BHIM (Bharat Interface for Money) launched by PM Modi on December 30, 2016. The UPI and BHIM apps were developed by the National Payments Corporation of India (NPCI) which is promoted by the country’s central bank- the Reserve Bank of India.

Now the RBI has launched a new Credit Card & UPI linkage scheme that will link UPI accounts to credit cards. RuPay, the card payment system of National Payments Corporation of India which now rivals American giants like VISA, Mastercard, and American Express in terms of the user base, will be the first one to access the facility of this scheme. This will revolutionise the credit card market of India and it even risks inviting doomsday for foreign card companies mentioned above.

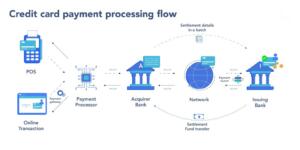

Currently, credit card companies have a well-defined revenue generation model. When credit money is transferred from one bank’s credit card to another, two types of intermediary players are involved. One is Razorpay, the payment gateway of merchants (because credit cards are used for people to do business transactions). Another player is the company providing credit cards like VISA, Mastercard among others.

In a transaction, Card provider and Bank share information to ensure that money is deducted from your account. After ensuring from the customer’s bank that everything is streamlined, the Card company tells the payment gateway company that the transaction is good to go. The gateway company then transfers the money to the merchant’s bank accounts.

All these processes take place within seconds. But, it costs a lot of money to make it look seamless. The customer’s bank and card issuing company together charge a small amount from the customers. Though the reasons they charge are different. Customer’s bank charges money because it is taking credit risk since it is entirely possible that the customer may not be able to repay in future.

On the other hand, Card company charges the transaction because it has established a huge infrastructure in order to carry out millions of such transactions every minute or so. They decentralise the cost-sharing and ask every consumer to pay a little. Combinedly both of these charges are known as Merchant Discount Rate (MDR). It is because the amount is deducted from Merchant’s bank account and involves anywhere between 1-3 per cent of total cost involved in the transaction.

In the case of RuPay debit cards, there is Zero MDR and merchants receive every single penny deducted from the customer’s account. The Modi government has set aside Rs 1,300 crore to pay compensation to the banks for RuPay and UPI transactions. The reason why similar incentives have not been provided to RuPay credit cards is because the majority of Indians are risk averse when it comes to spending money.

By the end of Financial Year, 2021, there were only 6.2 crore credit cards circulating in Indian geography. Compared to that, the number of Debit Cards is colossal to say the least. The numbers show that Indians cumulatively held 94 crore debit cards by the end of FY21. Given the fact that RuPay’s share in the card market is increasing at an exponential rate, (thanks to the financial inclusion initiative of the Modi government), this number will soon touch 100 crore.

But, RuPay is lagging in the credit card market. It does not make more than 25 per cent of total credit cards in India. However, its linkage with UPI is expected to boost its share. Currently, there are more than 5 crore merchants registered on UPI platform. Nearly 75 per cent of merchants engaged in trading all over India have QR codes for UPI payments. In terms of valuation, an average person to merchant transaction involves handover of Rs 769 to the merchant’s account.

The move to link the credit card information with UPI accounts would revolutionise open credit enablement as the banks and other financial entities would be able to offer micro-loans. The American credit card companies, which charge hefty fees for enabling credit as well as the debit transactions, will soon go out of business.

The UPI has already killed the payments dominance of the card players in the last five years. Now they are all set to lose the highly lucrative credit business as Rupay rises to the stature riding on UPI.

In the last few years, India has emerged as a global leader in the financial technology space. Many flow based lending companies like Slice, Uni, One are emerging and they mainly offer flow based lending which means giving loan based on the financial data of the user. (without any collateral)

The aim of this scheme is to become fully Aatmanirbhar in the financial space, from payments to lending. Today, the finance ecosystem is dominated by Indian companies due to the growing importance of software. While the Indian services companies like TCS and Infosys design the core software for global financial giants like Goldman Sachs, HSBC, Bank of America as well as the banking software for most of the central banks around the world, Indian product companies like Razorpay build the payments interface for them.

Now the time has come that Indian companies takeover the main service offering instead of just providing backend support like software and customer services. The success of UPI, which is being launched in many countries like France, UAE, Singapore, will put the Indian companies at the forefront of the financial services space.

In the pre-Modi era, the international digital transaction players like Visa, MasterCard and American Express were involved in oligopoly practices as they were the sole players. They used to charge customers an outrageous processing fee and had made card payments an elite practice.

The Modi government launched the country’s own digital payments system and built an infrastructure to encourage digital payments. And slowly India is emerging as a global leader in the whole finance space, the payments space is taken over and the next stop would be lending and wealth management.

Support TFI:

Support us to strengthen the ‘Right’ ideology of cultural nationalism by purchasing the best quality garments from TFI-STORE.COM

Also watch: