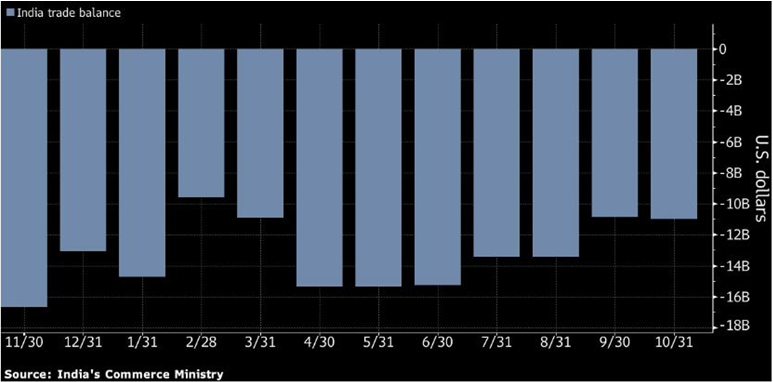

Riding on huge contraction in imports, the trade deficit of the country continues to decline. Due to muted demand, imports shrank by 16.31 per cent to 37.39 billion dollars while exports contracted by 1.11 per cent to 26.38 billion dollars. This has brought down the trade deficit to 11 billion dollars.

Experts see the contraction in exports as an obvious result of global slowdown. The global economic growth is estimated to be less than 3 per cent, lowest in a decade. “Negative exports for October have not come as a surprise, amidst global slowdown, particularly in the main destinations of Indian exports. However, the pace of de-growth for October has come down, month-on-month,” said EEPC India Chairman Ravi Sehgal.

Imports witnessed huge contraction, especially oil imports which accounts for almost one-fourth of the country’s total imports. Oil import fell by 31.74 per cent year on year to 9.63 billion dollars. The only sector to witness a jump in imports was Gold, where imports grew by 4.74 per cent to 1.83 billion dollars.

In the first six months of this fiscal year (April-October), exports shrank by 2.21 per cent to 185.95 billion dollars while imports were down by 8.37 per cent to 280.67 billion dollars. The trade deficit in the first six months was 94.27 billion dollars.

The Modi government’s flagship programme Make in India has made a significant impact on the Indian economy. Given the success of Make in India, export is growing as Indian products become more competitive in international markets. On the other hand, many products like equipment’s for India armed forces and smartphones are being manufactured domestically. This has helped the country to reduce imports figures and expand footprints of Made in India products across the globe.

India had near to zero presence in smartphone manufacturing before the Modi government came to power. Today the country is one of the largest manufacturers of smartphones with almost all major companies including Apple, Samsung, Xiaomi, and Vivo having plants in India.

The rise in exports, currency, and foreign institutional investors is very encouraging given the emerging markets across Asia are slowing down due to China’s woes. The imports and exports of China fell by double digit percentage points due to economic slowdown and trade war.

Riding on the significant drop in imports, India’s foreign exchange reached a record 448 billion dollars. The total foreign exchange reserves of India are almost 50 times greater than that of Pakistan. The debt-ridden country has foreign exchange of 10 billion dollars which is sufficient to cover only two months of imports.

India has more gold reserves than total foreign exchange reserves of Pakistan. India has gold reserves that are three times more than the total reserves of Pakistan.

The foreign exchange is growing due to an exponential increase in investment made by Foreign Institutional Investors (FIIs). The gap between exports and imports narrowed in the last few months, this is also one of the major reasons behind the rise in forex levels. The foreign investors are returning to India due to stable macroeconomic conditions and a full majority government.

India had forex reserves of $600 million in 1991 which were barely enough to cover three weeks of imports. We have come a long way from there and forex reserves have gone up by more 600 times since then. However, the foreign exchange of China is also many times more than that of India given its high export figures.

China posts a very high Current Account Surplus because its exports are larger than imports. The foreign exchange of China is almost 3 trillion dollars which is 7 times more than that of India. Export-led economies like China, Japan, Switzerland, Saudi Arabia, Russia, Taiwan, Hong Kong, and South Korea have greater foreign reserves than that of India.