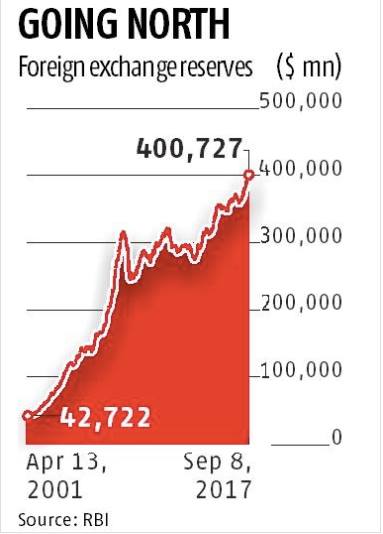

Amid the rising concerns of the expected slowing down of the economy which has been attributed to demonetisation and GST, India’s foreign exchange reserves have surged to an all time high of $400 billion. The reserves are held by the central bank of a country to pay its liabilities like the price of foreign imports. The reserves are held mainly in US dollars and in some cases in Japanese Yen. Forex reserves consists of foreign currency, official gold reserves and the special drawing rights granted by the Internal Monetary Fund(IMF). This figure alone is enough, to pay for all of the country’s imports for almost a year and it is safe to say that the economy will be able to withstand any unexpected changes rising from the global markets.

There was a time(1991) when India’s foreign exchange reserve would barely last two weeks and now India ranks eighth in foreign exchange reserves in a list which is headed by the likes of China(3.09 trillion) and Japan($1.2 trillion).

This record amount of reserves is mainly due to Foreign Direct Investment(FDI) in manufacturing as well as services and through the flow of funds from Foreign Portfolio Investors(FPI). The government received a lot of flak when the RBI data showed that almost all of the demonetised currency had returned to the central bank and which enabled the critics to wrongly label the demonetisation exercise as a failure and showed the subsequent slowing down of the economy in the latest quarter as ‘proof’ which signaled growing discontent and deteriorating faith of investors in India’s economy.

On the contrary, the latest surge of the foreign exchange reserves shows nothing but the strength of India’s macro economy and the continuing investor faith in growth. Foreign portfolio investments have been strong with equity investments at Rs 42,659 crore in 2017 and Rs 1.32 lakh crore going into debt. This has resulted in the rupee strengthening 6% this year, making it the best performer among major emerging economies.

(http://economictimes.indiatimes.com/…/articles…/60531270.cms)

The US central bank is expected to announce a reduction in stimulus later in the year which might affect the Indian economy adversely. The surge in India’s forex reserves is likely to help rupee withstand any volatility that may be seen on exodus of foreign funds from India’s debt and equity markets. In what can be seen as one of PM Modi’s biggest achievements, foreign institutional investors pumped in a whopping Rs.1 lakh crore into the Indian debt and equity market in the past 12 months alone.

The RBI started lapping up dollars aggressively since the rupee hit it’s lowest in August 2013 at Rs.67.78 a dollar due to the announcement of the rollback of the US stimulus programme. The Reserve Bank under former governor D Subbarao (who also happens to be a string critic of demonetisation), did not accumulate dollars, as it let the market forces determine an appropriate rupee value. That practice was reversed by Raghuram Rajan, who in his three years — up till September 2016 — added about $77 billion in reserves. Urjit Patel, the current governor, has stepped on the gas a bit more. In his first year, he has added about $30 billion in reserves so far. The rupee closed at 64.08 versus the dollar on 15th September,2017.

(http://indianexpress.com/…/forex-reserves-cross-400-bn-for…/)

However, market analysts are expecting a slowdown in FPI inflows. While the market witnessed outflows from the stock market in August and September, FPIs are close to reaching their debt investment limit and the FPI are expected to be significantly lower in the next quarter. However, the reserve is enough to face any potential threats which the slowing down of foreign investments might bring.

The strong forex reserve is now posing many management challenges for RBI. The swelling dollar corpus has meant a stronger rupee, hurting exports amid rising imports and posing currency management challenge for the central bank. The current account deficit (CAD) widened to 2.4% of gross domestic product(GDP) in the June quarter, up from 0.1% in the year-ago period according to the central bank. This figure is however much lower than what the market analysts expected to be which was over 3% of the GDP after demonetisation and GST. The currency appreciation is making imports more attractive while exports are becoming uncompetitive. The latest RBI data shows that the current account deficit, the excess of imports over exports, was at $14.3 billion in the June quarter, up from $0.4 billion a year earlier, and $3.4 billion in the March quarter.

(http://www.business-standard.com/…/india-s-forex-reserves-c…)

Economists expected the sudden surge in CAD due to the spike in gold imports prior to the introduction of GST responsible for half of the surge. The boost in forex reserves is due to the flow of capital and not trade surplus and hence money can go out the same way it came in, if the central bank doesn’t step in time and protect the rupee’s value albeit this time by selling dollars.

Inspite of the expected slowing down of the FPI in the next quarter, the rupee is expected to ascent to 61 versus the dollar by March and there’s a slight chance of rupee ascending to as high as 58 versus the dollar at the end of FY18. To overcome the hurdles faced by the limits on purchases of bonds and continue the flow of overseas funds, the government has lined up several high profile Initial Public Offerings(IPO) this fiscal year. Any US Federal Reserve action threatens to reverse the direction of the rupee’s movement and both the government and the central bank should takes steps well in advance to battle any subsequent volatility which would hit the Indian economy. Although the current reserve does provide a cushion to the policymakers to deal with sudden outflow of dollars.

The growing CAD can also be accounted to the fact that the Free Trade Agreement (FTA) is being misused by many countries leading to a surge in the gold imports. India’s gold imports have tripled to $15.24 billion, during April-August up from $5.08 billion in the same period, last year. The initial surge which was attributed to the GST continued in August which caught the government unaware. Gold came into India through some countries(Malaysia,Thailand to name a few) which India has a FTA with. The Gold came without any duty due to FTA clauses and only 3% IGST was charged. The recent surge came primarily via through South Korea which led to the government banning duty free imports from South Korea. Investigative agencies have found blatant violation of rules of origin especially in Thailand, which has led India to impose restrictions like raising the custom duty to discourage the inflow of gold which is hurting the economy. The government is also reviewing the option of excluding gold from any future Free Trade Agreements.

(http://www.livemint.com/…/Why-India-banned-gold-imports-fro…)

As the debate surrounding the onset of bullet trains continues to rage , there is little doubt that PM Modi is atleast a disruptor if not a dreamer. He is following the footsteps of Franklin D. Roosevelt who ended USA’s fascination with gold, Modi too is trying to fundamentally change the way how the Indian economic system thinks and operates with exercises like demonetisation, GST, electric vehicles and now bullet trains.