Currently, one of the biggest crises facing the Indian banking sector is NPA. We are working on a detailed research-oriented write-up on the same, however, the focus of the current article is trying to figure out an innovative / radical solution to ~INR 1.10 Lakh crore funding deficit in the PSU Banking system in India. The Government of India has pledged to infuse INR 25,000 cr., in the Indian banking system. However, the degree of efficacy of the same cannot be estimated. In fact, the kind of ruckus in the Indian bank books is difficult to forecast. This article does not focus much on the causes of NPA, the status of NPAs, among others; but on few radical solutions in NPA in light of developments observed in the current IDBI Bank deal.

From an investor perspective, buying any bank like say IDBI Bank is fraught with risk, because one does not adequately know the risky / sticky assets before-hand. In fact, a detailed due diligence and diagnostic review is a MUST prior to committing on the investment; which will not work much in favor of the bank. I have been following Dr. Viral Acharya (the new Deputy Governor) of RBI and feel his addition to the RBI is a welcome relief to the overall NPA crisis in India; however policy decisions take sweet time and government has not shown adequate emergency / mission mode activity in dealing with NPA crisis.

Having said that, we believe selling off or privatizing PSUs at the current level is not right. One, because they have too much of bank books and second, they won’t fetch the required valuation. Further, PSU banks function as backbone for finance commodity industries like cement, steel, etc., which would not be touched by private banks. Hence, selling off is not a right option, nor divesting stake is an option. We suggest a three pronged approach at clearing the capital deficit problem in banks:

- Carving out a real-estate REIT entity and raising funds

- Separating the CASA / infrastructure portfolio and raising funds

- Attacking the Assets into Sustainable & Unsustainable

Carving out a real estate entity specifically a REIT

Our current article focuses on the REIT portion. A REIT is acronym for a Real Estate Investment Trust. Simply put, it is a company / investment vehicle which owns real estate, that is leased out. So, the income of the REIT entity is the lease rental it derives in the property less the maintenance expense it has to incur for the same. The biggest real estate that the PSU banks hold are its branches and offices at key locations. We believe these assets are the crown Jewel in the books of the PSU. Ideally, these must be carved out and sold to a REIT and in turn the bank shall receive hefty money for such sales and these branches / offices shall again be taken by the bank on long term, say 25 year, lease / rent. This will ensure that there is no disturbance in the existing banking operations; and at the same time the banks are able to raise fresh capital.

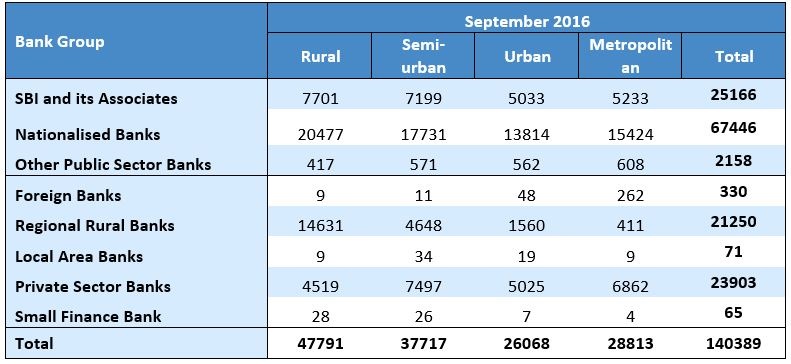

In order to get the branches data, we look at the RBI database and came up a macro number of branches segregated into their region-oriented location as under:

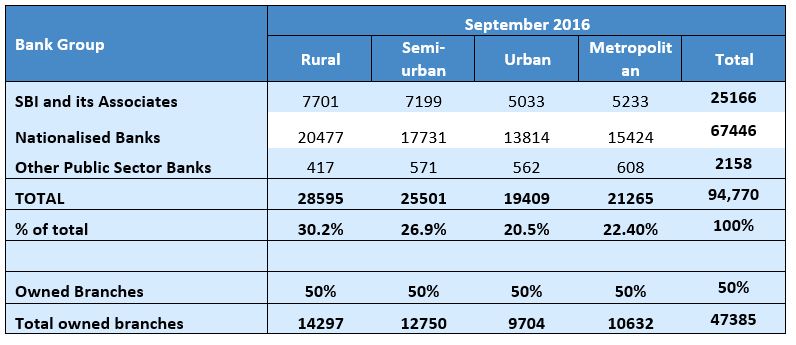

The first three line items i.e. SBI & Associates, Nationalized Banks & Other PSUs account for 94,770 bank offices (branches and working offices) in India. Lets take them out of the above table below:

A peculiar observation, in the bank branch / office location is that the rural banks account for only 30.2% of the total branches, while the balance chunk is non-rural. In fact, the urban and the metropolitan locations account for 42.9% of the total branch locations.

Now, in the above table I have assumed that of all the total branches, ~50% are owned branches. I was unable to get a statistical break-up at RBI site showing details of owned & leased branches / offices. However, since PSU banks are old generation banks, they preferred owned model then leased model; which ensure continuity in the operations rather than changing the office multiple times.

Having said that, I propose that these say ~47385 offices / branches of the Banks should be carved out and transferred to separate real estate company. What could be the value of such bank assets? I used a conservative approach at estimating the value of these assets:

I have taken a Rs. 5000 per sq. ft., valuation of the real estate properties. Now, this value of Rs. 5000 is less, given than all the banks have their regional offices in extremely prime areas. In fact, the Nariman Point, Mumbai is filled with full 20 storeyed bank buildings.

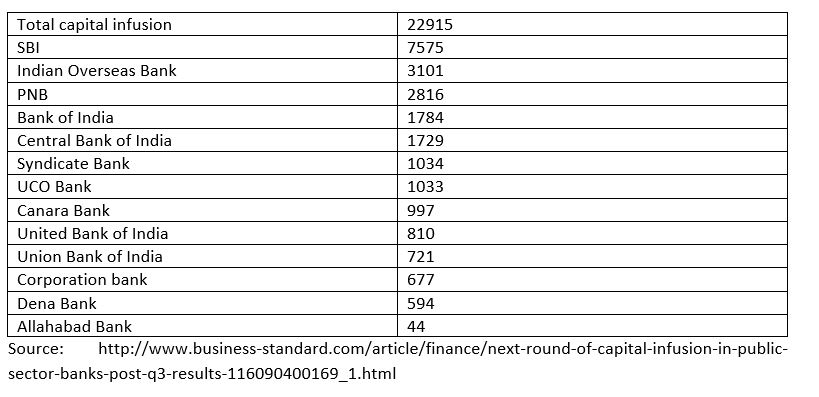

How much money has the Government pumped in PSUs and what is their responsibility?

A per Business Standard article dated 4th Sep 2016, the Government of India has pumped in ~INR 22915 cr., in PSU banks as under:

Further, as per the article states, “under Indradhanush roadmap announced last year, the government will infuse Rs 70,000 crore in state banks over four years while they will have to raise a further Rs 1.1 lakh crore from the markets to meet their capital requirements in line with global risk norms Basel-III”.

If we take these two data-points i.e. a) the funding requirement of INR 1.1 L cr. as envisaged by Government , and b) our conservative working of ~1.18 L cr., we believe this presents a unique opportunity for banks to raise money. Undertaking this one time activity will lead to huge capital infusion in the banks without disturbing its operations. A detailed valuation report, title search report, lease / rent yield opportunity, viability needs to be carried out. But, what are speaking of are broad strokes and an idea to re-vitalize the process.

This solution does face many issues which include; raising such capital is the VOLUME. Expecting investors to pour in money to such an extent is difficult. In fact, in USD term this amount translates to USD 17.2 bn. So, ideally the Government of India (via LIC, GIC, etc.) should act as an anchor investor in this REIT fund with by footing in ~50% of the total value, while balance should be raised from pension funds. Now, this investment in the real estate asset is relatively risk free as the investor is not bothered about the banks functioning. You may wonder, how does an investor benefit? The investor will look to make Dollar Denominated Rental Yield of ~6% (net of currency hedge) in India. Which technically means, that the rent of the REIT should be such that it earns 10% annual return to the investors. Further, the government may list such REIT entity in either Indian stock exchange or Singapore Stock exchange. DLF has already done for its rental asset portfolio.

The appetite such capital exists for India, funds like Brookfield Capital have USD 1 bn fund with SBI for its NPA assets. This kind of deal will be win-win for banks and the investors as well the overall banking sectors.

Few operational issues which can create problems are a) payment of state government / local government stamp duty and b) capital gain. The Central Government will have to pass an ordinance exempting such transfer of asset from capital gain and stamp duty. This will boost investor confidence and reduce unnecessary outgo of cash.

We believe radical and innovative financial solution is the key to reviving the Indian banking system. Indian PSU banks are backbone of India’s economic growth and the problems they face are real and need immediate attention. In the next article on NPA, we focus on the CASA / infrastructure portion.