Writing an article on Dr. Urjit Patel or Dr. Rajan is a daunting task. One of the most important thing is that there is always so much that gets published, your ability to surprise the reader with new insights is limited. We look for fresh insights; its been almost a month, since Dr. Urjit Patel has been announced as a successor to Dr. Rajan; and there are already plethora of articles talking about him with how is the best successor for Dr. Rajan.

There are news in media stating that Dr. Urjit Patel was first choice as RBI Governor for PM Modi. From a political perspective, it’s a wise move given that Dr. Urjit Patel is an RBI internal, so there is limited scope for Opposition from the media. Moreover, Dr. Urjit Patel comes with an inflation hawk kind of attitude, so again; this works in favor everyone who is opposed with rate cut, among others.

So, we have decided to touch on multiple pointers as under:

- Urjit Patel’s: Reflections from research papers

- Insights on Inflation from the Monetary Policy Report

URJIT PATEL: REFLECTIONS FROM RESEARCH PAPER PUBLISHED

One very insightful article on Dr. Urjit Patel was that by LiveMint, wherein they went through some of Dr. Patel’s policy papers to see his views and perspectives. I loved that idea; there is no point talking about someone’s CV. I believe that’s the best way to look at Dr. Patel, is by analyzing his work. We went in a bit more into details and tried to come with more understandings.

Insights from Dynamics of Inflation “Herdings” by Gangadhar Darbha & Urjit Patel 2012

The paper was published probably in the tenure of Dr. Subarrao, the opening lines of the report were quite harsh towards his role and went on to lament the role of Central Banker. Dr. Subbarao stated that with Food & related items being ~46% to 70% of the total inflation basket, it is difficult as policy maker to focus on inflation from the supply side factors. This sentence was peeled in the report with three stark observations:

- Inflation is primarily driven by petroleum & food prices; however removing these two components would be better for inflation targeting which would then free the central bankers from targeting the same.

- It is impossible to know which is the right price index in India to target; given its vastness.

- The Central Bankers and the policy makers are happy with targeting WPI as the inflation index, which makes life easy for them.

The paper then goes on to statistically deconstruct the Inflation in India, via multiple econometric model wherein it concludes:

- Inflation originates not just from food & petroleum but is rampant across the sector

- Overall and core inflation factors have further hardened which will, lead for higher inflation in the forthcoming period

- Common factors influencing inflation has increased over the years; thus singling out since item is difficult

The reason for giving an insight on the said report is it served as pre-cursor to Dr. Patel’s 2014 report a deputy governor of RBI, titled ‘Report of the Expert Committee to Revise and Strengthen the Monetary Policy Framework’. The opening page of report mentions key pointers from Dr. Rajan as under:

The primary role of the central bank, as the RBI Act suggests, is monetary stability, that is, to sustain confidence in the value of the country’s money. Ultimately, this means low and stable expectations of inflation, whether that inflation stems from domestic sources or from changes in the value of the currency, from supply constraints or demand pressures.

I have asked Deputy Governor Urjit Patel, together with a panel he will constitute of outside experts and RBI staff, to come up with suggestions in three months on what needs to be done to revise and strengthen our monetary policy framework. A number of past committees, including the FSLRC, have opined on this, and their views will also be considered carefully.

MOVING TO: INSIGHTS ON INFLATION FROM THE MONETARY POLICY REPORT

With this background, let’s look at key observations and recommendations from the report.

The Committee recommends that inflation should be the nominal anchor for the monetary policy framework. This nominal anchor should be set by the RBI as its predominant objective of monetary policy in its policy statements. The nominal anchor should be communicated without ambiguity, so as to ensure a monetary policy regime shift away from the current approach to one that is centered around the nominal anchor. Subject to the establishment and achievement of the nominal anchor, monetary policy conduct should be consistent with a sustainable growth trajectory and financial stability.

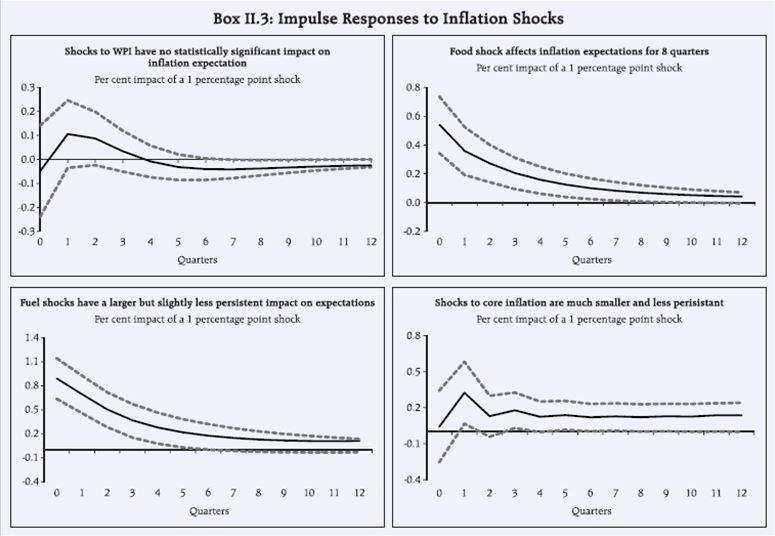

The above charts reproduces from the report, are very pertinent. The most important point is a sensitivity analysis revealing impact of a 100 basis points (bps) shock on each type of inflation as under:

While, the % contribution of the Food & Fuel factor is ~57%, whether a revised CPI index with less than 50% but more than 40% needs to be explored. For example, as per the report Brazil has 40% share of food & fuel. However, I believe there needs to be a more detailed NSSO survey to see what is the contribution of the Food & Fuel spending in the overall spending in individuals with a higher sampling across the country and varied income profile. Some of issues of only CPI targeting; it may keep the cost of capital higher in the country. With higher interest rate, a simple CAPM model,

Ke = Rf + β(Rm – Rf)

The Rf which drives the formula is risk free return, with higher Rf, the Ke i.e. cost of equity of the nation will always be higher. Purist may point to basic inflation / currency formula. This can be a bit lopsided, but the point in business I would like to drive here is that RoE i.e. Return on equity should always exceed Ke, so higher will Ke, will demand businesses make more money than the cost of equity.

I believe study on this line will be critical in understanding the impact of Inflation, Interest rate & IRR expectations coupled with impact of GDP. Basically, marrying of these factors is critical and can be a topic for next article. I should have completed my CFA, it would have helped.

Moving on, to Inflation targeting

Despite what is made out as Dr. Urjit Patel as an inflation hawk, the monetary policy report, has given the below timeline for Inflation Targetting:

- Range: The Committee recommends that the nominal anchor or target should be set at 4% with a band of +/- 2% around it:

- in view of the vulnerability of the Indian economy to supply/ external shocks and the relatively large weight of food in the CPI; and

- the need to avoid a deflation bias in the conduct of monetary policy.

- Time horizon: This target should be set in the frame of a two-year horizon that is consistent with the need to balance the output costs of disinflation against the speed of entrenchment of credibility in policy commitment.

- Target tenure / step approach: Gradual move starting with to

- Reduce inflation from 10% to 8% over a period not exceeding the next 12 months

- Reduce from 8% to 6% over a period not exceeding the next 24 month

- Post this period; formally adopt the recommended target of 4% inflation with a band of +/- 2 per cent.

- Transition path should be clearly communicated to the public.

The point above 3.d. is not adequately communicated, in fact, given this situation, we see always financial journalists stating that the interest rate reduction will depend on CPI moderating to 4%. However, given the inflation currently hovering at ~6%; there is scope interest rate reduction.

Reuters is already reporting that there is need to appoint the Government nominees on the Monetary Policy Committee; whose meeting is scheduled on Oct 4th. RBI and the Government shall each have three representatives on the committee, with the RBI’s being the Governor and the two most senior monetary policy officials.

A good monsoon, uptick in manufacturing PMI, coupled with Seventh Pay Commission, there is potential for rate cuts. RBI and the Government panel needs to get its house in order. Already Nirmala Sitharaman and Nitin Gadkari have echoed for rate cut, with Nitin Gadkari stating that there is need for at least 2% rate cut. Economists were highly dismissive of the same; and a 2% cut would be too arbitrary and high; there remains room for further cut.

Let’s see how things pan out for the Economy.

PS: We are working on a write up on NPA and some pointers from RBI Annual report

Notes & Sources:

http://www.livemint.com/Politics/l8jZkafA1fMSvnpqjaspQK/THE-ECONOMICS-OF-URJIT-PATEL.html–

DYNAMICS OF INFLATION “HERDING”: DECODING INDIA’S INFLATIONARY PROCESS paper by Dr. Urjit Patel & Gangadhar https://www.ciaonet.org/attachments/19932/uploads

Motilal Oswal EcoScope: http://www.motilaloswal.com/site/rreports/636074645091589687.pdf

http://in.reuters.com/article/india-rbi-patel-idINKCN11B130